GPT-Powered Stock Trading Research

Can a large transformer model act as an all-in-one, news-based trading bot? A senior research project.

Background

Back in the dark ages (yes, I mean before Chat-GPT took the internet by storm), transformer-based text generation models were known only to AI researchers and the nerdiest of programmers. It took until the release of OpenAI's GPT-2 in early 2019 before I joined the hype train. Like everyone else at the time, I wanted to co-opt the power of transformers for fun and profit, but alas OpenAI was only allowing other big-time researchers, or deep-pocketed corporations access to their groundbreaking technology. Thankfully in the meantime, Ben Wang and Aran Komatsuzaki were assembling a crack team of open-source gods to compete with OpenAI. Working at breakneck pace, they released GPT-J, a free and open competitor to GPT-2 and GPT-3 by early 2021, just in time for me to make use of their work in my senior research project for my college degree.

Timeline

My Research Project

Concept

In mid-2021, there was lots of excitement around the flexibility of large transformer models. I wanted to see if I could use GPT-J as an all-in-one news-based trading bot. The idea being, if a model has read enough of the internet as background, it should understand the context of a news article, and output a trading signal for a given company.

Input: News article about a company ⮕ Output: Buy/Sell/Neutral signal

Data gathering

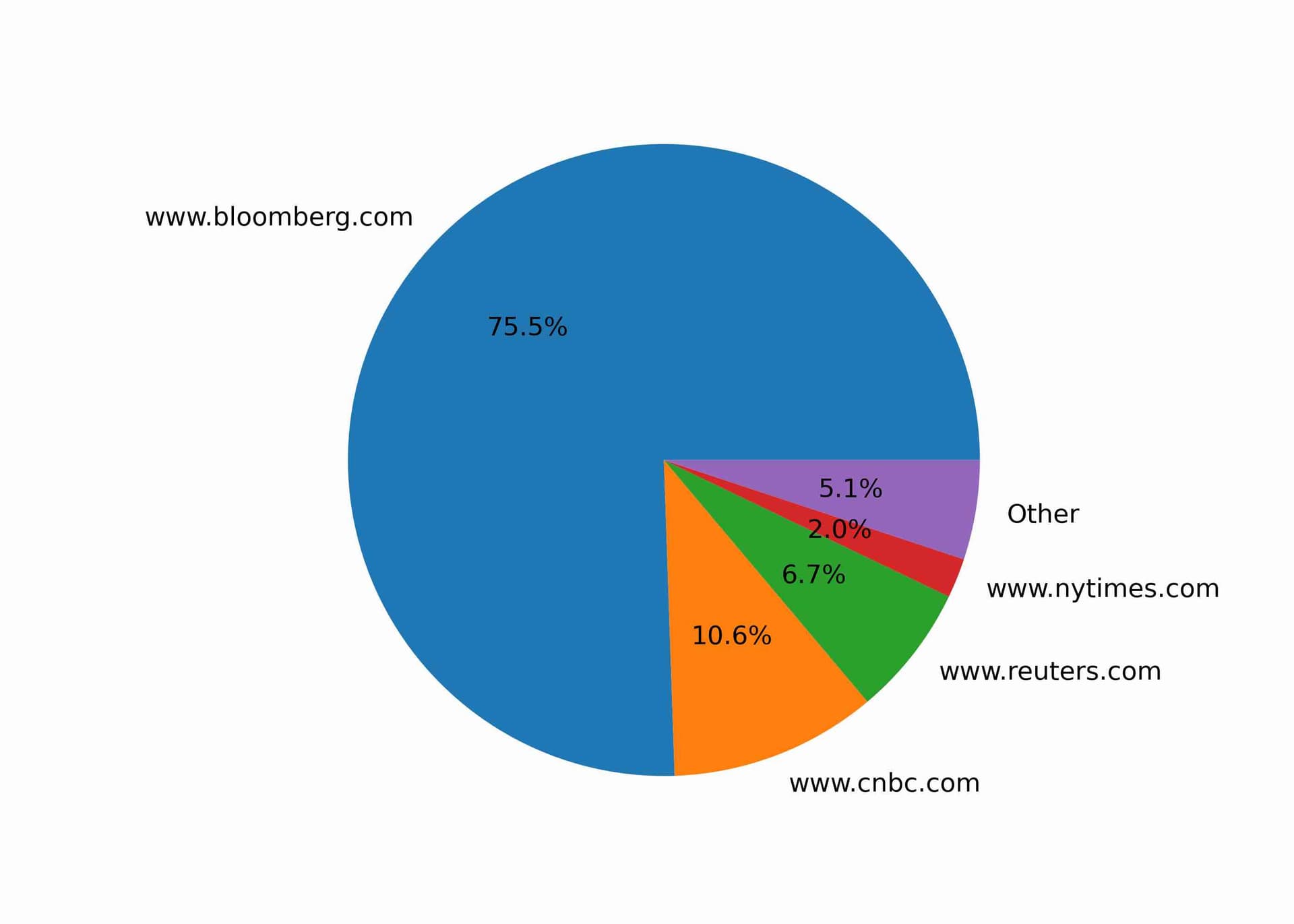

For the best chance of success, I decided to fine-tune the GPT-J-6B model with data formatted like the prompts I intended to test with. I scraped and labeled 140,000 news articles from the below web sources:

To avoid rate limiting, I created a custom web scraper to use and manage a pool of rotating proxies. I also used a custom rate limiter to ensure that I was not making too many requests to any given domain. Running the scraper from an OracleVM, I was able to scrape around 40 articles per minute and complete all 140,000 articles in around 2.5 days.

class Scraper:

"""

Scrapes a list of seed urls and calls the parser function to process each result.

The parser function should accept two arguments: the response object and the url.

The parser may pass a list of new urls to scrape with the addUrls(urls) method.

The scraper attempts to never scrape the same url twice.

"""

def __init__(self, seedURLs = [], parser = None, options = None):

emptyLogFile()

self.options = {

'cookieDirectory': './cookies/',

'scrapeThreads': 10,

'rateLimits': {},

'maxAttempts': 3,

'proxyUpdateInterval': 10

}

if options:

self.options.update(options)

self._cookies = loadCookies(self.options['cookieDirectory'])

self._parser = parser

self._urlQueue = queue.PriorityQueue()

self._finishedUrls = {}

self._finishedUrlsLock = threading.Lock()

self.addUrls(seedURLs)

self._threadNumber = self.options['scrapeThreads']

self._proxySessions = queue.Queue()

for proxy in self.verifyProxies(self.getProxies()):

self._proxySessions.put(proxy)

self._rateLimits = {}

self._rateLimitsLock = threading.Lock()

for domain in self.options['rateLimits']:

self._rateLimits[domain] = {

'limit': self.options['rateLimits'][domain],

'lastRequest': {}

}

def addUrls(self, urls):

""" Adds a list of urls to the list of urls to scrape. """

count = 0

with self._finishedUrlsLock:

for url in urls:

if url not in self._finishedUrls:

self._urlQueue.put((0, url))

count += 1

def run(self):

""" Starts the scraping threads and the proxy maintenance thread. """

scrapingThreads = []

for i in range(self._threadNumber):

t = threading.Thread(target = self._scrape)

t.start()

scrapingThreads.append(t)

proxyMaintThread = threading.Thread(target = self._maintainProxies)

proxyMaintThread.start()

for t in scrapingThreads:

t.join()

proxyMaintThread.join()

successfulScrapes = len([v for v in self._finishedUrls.values() if v])

print(f"Finished scraping. {len(self._finishedUrls)} urls scraped. {successfulScrapes} successful scrapes.")

I then split my dataset into a training set with 90,000 articles and into validation/testing sets with 10,000/40,000 articles respectively.

Training

Because the model weights are over 60GB, specialized computing was required for this training task. The training was done with a Google TPU-v3 generously donated by Google's TPU Research Cloud. I trained my model using the following hyperparameters:

{

"layers": 28,

"d_model": 4096,

"n_heads": 16,

"n_vocab": 50400,

"warmup_steps": 160,

"anneal_steps": 1530,

"lr": 1.2e-4,

"end_lr": 1.2e-5,

"weight_decay": 0.1,

"total_steps": 1700,

"tpu_size": 8,

"bucket": "peckham_tpu_europe",

"model_dir": "mesh_jax_stock_model_slim_f16",

"train_set": "stocks.train.index",

"val_set": {

"stocks": "stocks.val.index"

},

"val_batches": 5777,

"val_every": 500,

"ckpt_every": 500,

"keep_every": 10000

}

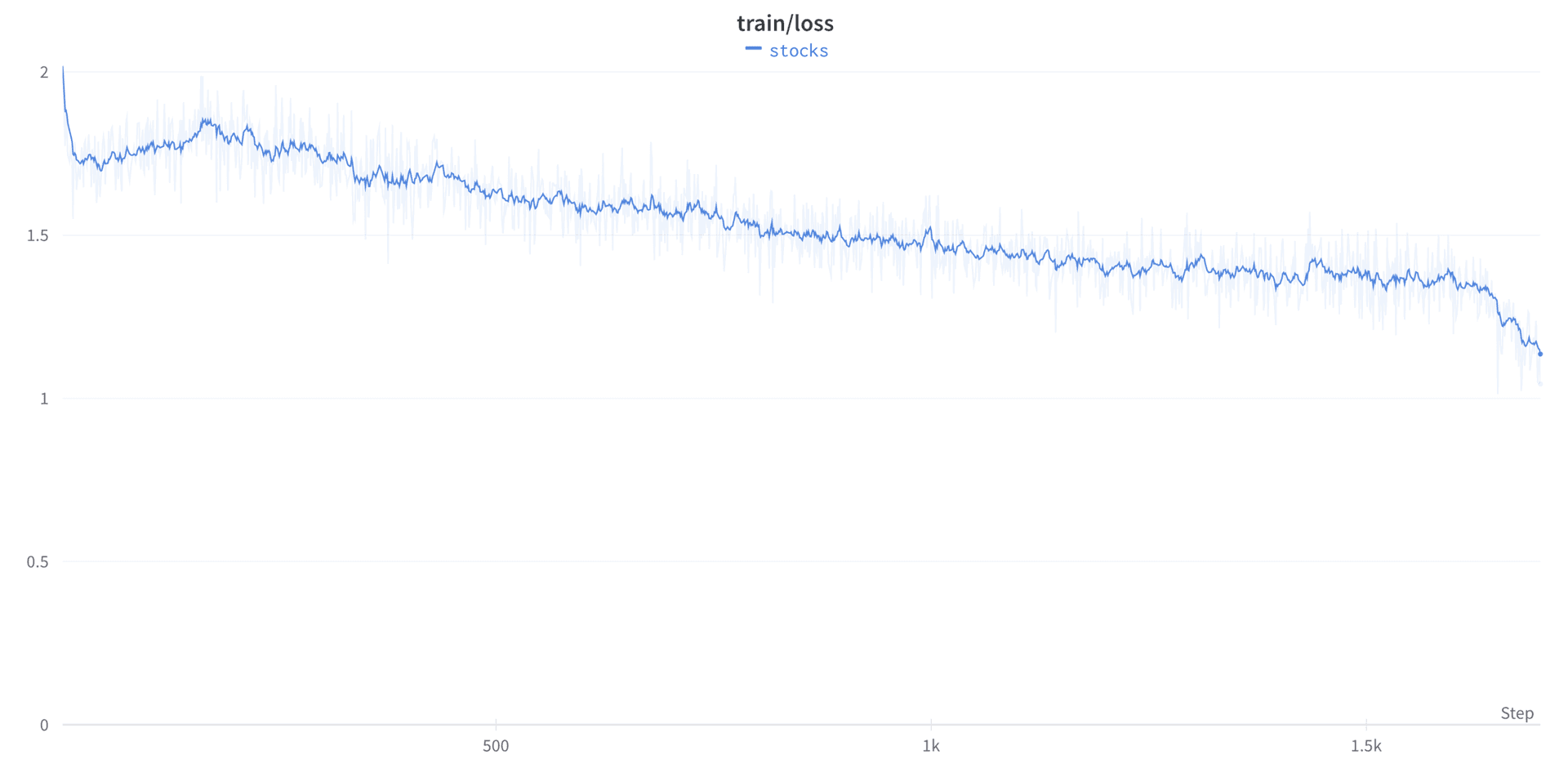

Training Loss

At first, I was encouraged by seeing a meaningful decrease in training loss, however, now I believe this was due to overfitting to the training set.

Results

Fine-tuned model: 50.58% (N=40K) correct guesses of stock price movement direction.

Standard GPT-J model: 50.63% (N=40K) correct guesses of stock price movement direction.

Human testing: 56% (N=120) correct guesses of stock price movement direction.

Conclusion

In my testing, GPT-J performs no better than random when predicting the direction of price movement based on a news story. Furthermore, fine-tuning the model does not improve prediction accuracy.

I believe these results are due to the following factors:

- The model (except for a small amount of fine-tuning) is not trained on financial data.

- The data was not cleaned well enough to remove noise.

- Text data is not a good representation of financial data. In other words, the model doesn't care about the actual numbers, only how well they "sound" in the context of the article.

- The articles may also not have enough information to predict price movement anyway. News is often considered a lagging indicator of price movement, and the articles I scraped were often published after the relevant price movement had already occurred.